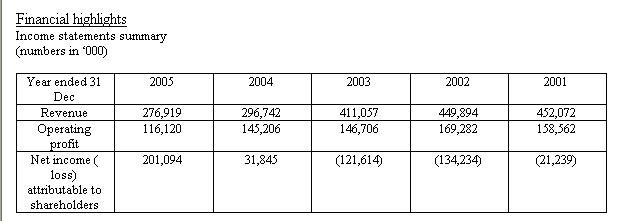

Net income has in 2003 to 2001 has been negatively impact by deficit in revaluation. However, situation has improved as the economy recover in 2004 to 2005. Revenue has fallen dramatically as the company has sold off a substantial amount of its non-property business.

*UOL equity investment Pte Ltd deemed interest is derived from the shares it held Through United Overseas Bank Nominees.

United Overseas Land Limited deemed interest is derived from both shares it held through United Overseas Bank Nominees and its stake in UOL equity investment.

United overseas bank deemed interest is derived from share it held via Tye Hua Nominees.

Mr. Wee Cho Yaw deemed interest is derived from the 700,000 shares he held and his stake in Haw Par Capital Limited, Straits Maritime Leasing Private Limited, UOL equity investment and United Overseas Land Limited.

Telegraph Development Limited deemed interest is derived from shares it held via United Overseas Bank Nominees, CIMB-GK securities and Oversea-Chinese Bank Nominees.

JC Summit Philippines Limited, JG Summit Holding Inc.and Mr. John Gokongwei Jr all derive their deem interest from their direct and indirect stake in Telegraph Development Limited

Valuation

Scenario 1

From 2001 to 2005, Singapore economy has roughly experience one business cycle, from the economic recession in 2001 to the recovery in 2003-2004. The average result is indicative of the result expected in future business cycle

As of present, based on current economic characteristics, the estimated worth of the company is S$1.67 per share.

Scenario 2

Allowing for a conservative growth of about 4% for next 3 years may not seem too speculative.

Using the above conditions, the company will be estimated to worth about S$ 3.65 per share.

Recommendation

Valuation

From the DCF analysis, UIC is a worthwhile investment in both scenario.

Specific Trends

The major trend that is happening in property market in Singapore is Real Estate Investment Trust (REIT). REITs have been well received by investors in Singapore and are a good way to unlock shareholder value. Recently, Ascott group offer its REIT to its shareholder at a discount price of S$0.68. The REIT is now trading at about S$1.08. If this were to happen to Singapore Land then the investment will be very profitable. In addition, recently major shareholder John Gokongwei Jr. tries to takeover the company in order to implement its REITs plan. This increases the likelihood of the implementation of REITs for UIC. UIC has a larger property portfolio than Singapore Land and possibility of REIT implemented via UIC is higher than Singapore Land.

Conclusion

It is recommended to have buy rating for UIC for now.

Comments